The European Union's planned issuance of €750 billion in bonds to fund its recovery program will create a major new player in bond markets for the long term, and it could also ease pressure on the "doom loop" that has bedevilled weaker EU banks and economies, according to market participants.

EU leaders reached an agreement in July to establish a coronavirus recovery fund offering €390

billion in grants and €360 billion in low-interest loans to

pandemic-stricken EU countries. The EU has departed from its previous

policy of not financing deficits and will borrow in the commercial

markets to finance up-front transfers.

"By issuing debt in the market on this scale, the

EU also provides the ECB, as well as investors, with a new liquid

euro-denominated benchmark instrument benefiting the euro's status as a

reserve currency," said S&P Global Ratings.

The EU's scheme to fund the coronavirus recovery

package by issuing bonds on a major scale for the first time will create

a long-term, triple A-rated debt security for institutional investors,

said Nicola Mai, portfolio manager and sovereign credit analyst at

Pimco, an investment management company.

"This is a very significant step because for the

first time the EU has got common bonds to finance cross border

transfers," he said.

"This bond has not come to the market yet, but we think it will trade close to where EU bonds trade at now."

Only Germany and the Netherlands currently have a

Triple-A rating in the EU, but the EU bond is expected to be Triple-A

rated, too, said Mai, who also expects the bonds to be refinanced over

the long term.

"The EU is rated triple A by two of the big rating

agencies. I would think the EC has been in contact with the rating

agencies to establish a system to satisfy the agencies in order to keep a

very high rating. There are not a huge amount of safe assets around in

Europe and the true safe asset is the German bund, but it is hard to see

the EU defaulting. There is a decent chance these bonds will be rolled

over in the long-term, too," he said.

The European Commission is empowered by the EU

Treaty to borrow from international capital markets on behalf of the EU.

This is not the first time that the EU has issued bonds — indeed it

currently has three loan programs to provide financial assistance to

countries with financial difficulties and all three are funded through

bonds — but it has never before done so on such a scale. These EU bond

maturities will be repaid after 2027 and by 2058 "at the latest," said

the EU, and the bulk of the sum will be borrowed between 2020 and 2024.

'Step towards fiscal union'

EU government debt at the end of last year stood

at more than €10 trillion, of which debt securities accounted for 80.9%

of eurozone and 80.6% of all EU member states' government debt.

"The issuance of common debt is a step towards

fiscal union and opens a box that many more fiscally conservative

countries had sought to keep closed. Despite protestations now, future

EU budgets may see greater use of borrowing and methods of repaying the

debt will need to be agreed," said Oliver Blackbourn, portfolio manager

on the multi-asset team at Janus Henderson, via email.

The EU's bond issuance will also ease political

pressure on the ECB, said Blackbourn, by providing a less politically

fraught source of government bonds for it to purchase. The ECB's capital

comes from national central banks and is calculated using a key that

reflects each country's share of EU output and population. It can buy up

to 50% of debt issued by supranational institutions. The ECB has

announced plans to purchase almost an extra €1.5 trillion of bonds in

response to the coronavirus pandemic in addition to the €2.6 trillion it

already owns.

"Purchases of German bunds have always represented

a major challenge for the ECB as Germany is the largest subscriber to

the capital key but has been relatively conservative in its issuance of

debt," said Blackbourn.

"With the ECB self-imposing limits on how much of

each issue it can buy, German bunds have always been most likely to hit

the limit first. Any deviation from the capital key is a source of

tension with the fiscal hawks on the ECB's governing council."

Germany represents 18% of the ECB's capital key

and has more than €1.3 trillion in bunds outstanding. France, Italy and

Spain have larger outstanding debt piles and smaller contributions to

the capital key so are less likely to run into the ceiling per issue,

said Blackbourn.

"While all major European nations are issuing more

debt to deal with the pandemic, a common debt instrument that avoids

the political frictions of buying individual country debt should remove

an ongoing headache at ECB discussions, at least for a time," he said.

Doom loop

The EU's bond issuance provides an alternative

asset class for financial institutions to invest in that are not linked

to a single country. This potentially reduces the influence of "the doom

loop," whereby banks hold their sovereign nation's bonds and so drag

each other down in the event of a crisis.

Banks can assign a zero risk weighting to

sovereign bonds but this has long been controversial since it encourages

banks to increase their stock of sovereign debt. This increases the

risk of the doom loop being enacted as weak banks can destabilize their

home nation's governments, while governments in trouble can push their

banks over the edge. It is an issue which has dogged weaker European

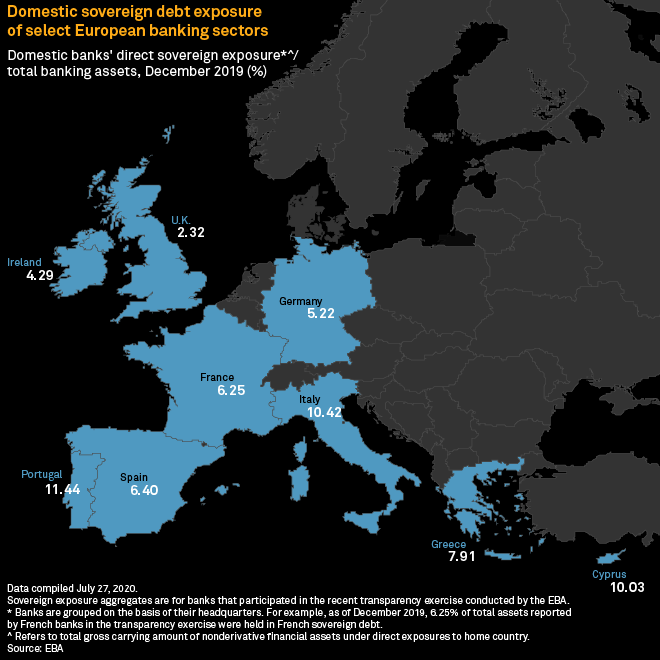

economies such as Italy, Greece and Portugal. For instance, Portugal has

nearly five times the rate of domestic sovereign bond holding than the

U.K., with Italy not far behind.

Jacqueline Mills, managing director at the

Association for Financial Markets in Europe, has said creating a

substantial market in EU bonds could relieve pressure on the doom loop,

though she warned that this was likely to take some time.

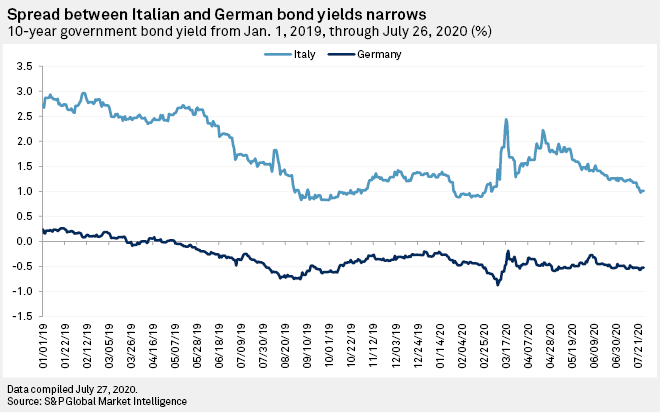

Mills also noted that the spread between German

bunds and Italian bonds narrowed after the EU's rescue package

announcement. German bunds have long been viewed as Europe's primary

safe asset, so much so that yields on 10-year bunds are negative, though

the spread between German and Italian bonds has narrowed over the past

18 months as the Italian government stabilized.

Christian Edelmann, co-head of EMEA financial

services at financial services consultancy Oliver Wyman, also said the

EU's bond issuance scheme would aid a lessening in pressure of the doom

loop.

"It's a step in the right direction towards

reducing the doom cycle, it provides a way for banks to diversify their

portfolio, to provide them with a more balanced portfolio since they can

invest in an asset class not linked to one country," he said.

Mai, too, viewed the EU's rescue package as likely to be positive in the long term for reducing the strength of the doom loop.

However, Fitch Ratings said measures taken by the

ECB during the pandemic, with its targeted long-term financing

operations now offering funding at negative rates, could see banks

increase their sovereign exposure.

S&P

© S&P - Standard and Poor

Key

Hover over the blue highlighted

text to view the acronym meaning

Hover

over these icons for more information

Comments:

No Comments for this Article