|

|

Following a drop in the first quarter of 2020, the aggregate capital ratios for significant institutions, (i.e. banks that are supervised directly by the ECB) increased steadily throughout the remainder of 2020. The aggregate Common Equity Tier 1 (CET1) ratio stood at 15.62% in the fourth quarter of 2020, the aggregate tier 1 ratio stood at 16.95%, and the aggregate total capital ratio stood at 19.51% (up from 14.94%, 16.13% and 18.60% respectively in the fourth quarter of 2019). Aggregate CET1 ratios at country level ranged from 12.91% in Spain to 29.14% in Estonia. Across business model categories as applied in the Single Supervisory Mechanism, global systemically important banks (G-SIBs) reported the lowest aggregate CET1 ratio (14.46%) and development/promotional lenders reported the highest (32.09%).

The aggregate non-performing loans (NPL) ratio fell to 2.63% in the fourth quarter of 2020. The stock of NPLs declined by 12.4% in one year, falling from €506 billion in the fourth quarter of 2019 (last reporting date before the outbreak of the pandemic) to €444 billion in the fourth quarter of 2020. At country level, the average NPL ratio ranged from 0.78% in Luxembourg to 25.54% in Greece. Across business model categories, custodians and asset managers reported the lowest aggregate NPL ratio (0.35%) and diversified lenders reported the highest (5.74%).

The annualised return on equity (RoE) stood at an aggregate level of 1.53% in the fourth quarter of 2020 − down from 5.16% a year earlier. This development was driven by a decrease in aggregate net profits, mainly attributable to a significant increase in impairments and provisions and a fall in operating income.

The aggregate liquidity coverage ratio rose continuously in 2020, standing at 171.78% in the fourth quarter of the year (up from 145.93% in the fourth quarter of 2019). The upward trend compared with a year previously was driven mainly by a significant increase in the aggregate liquidity buffer, in particular during the first three quarters of 2020.

With this data release, the ECB is publishing statistics on cost of risk for the first time. Cost of risk is the ratio of the adjustments in allowances for estimated loan losses during the relevant period (annualised) divided by the total amount of loans and advances subject to impairment. The aggregate cost of risk for significant institutions increased during 2020, reaching 0.67% in the fourth quarter, up from 0.50% a year earlier.

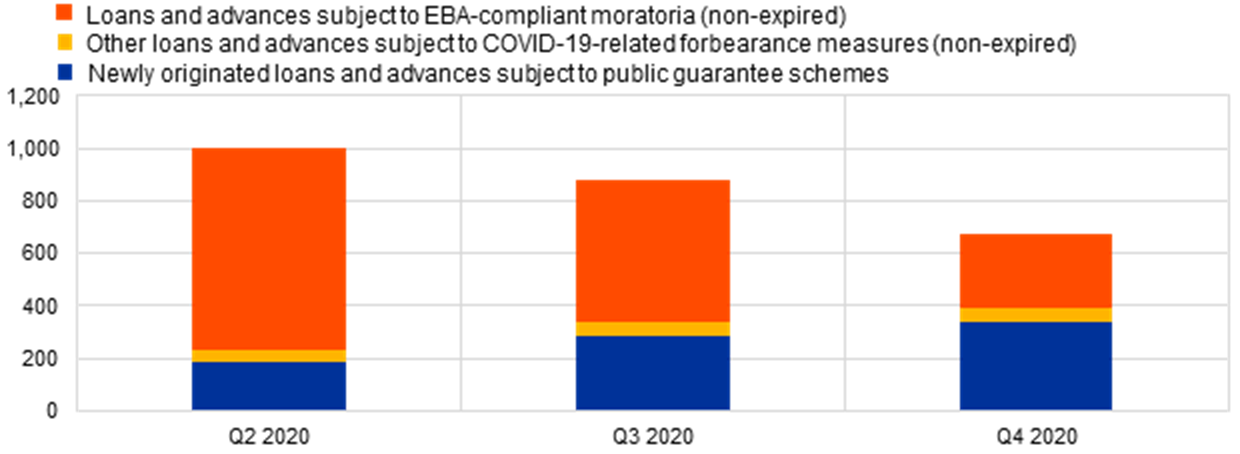

In response to the outbreak of the coronavirus (COVID-19) pandemic, data on loans and advances subject to COVID-19-related measures have been collected on the basis of reporting standards developed by the European Banking Authority. In the fourth quarter of 2020 non-expired loans and advances subject to EBA-compliant moratoria decreased to €282 billion, from €766 billion in the second quarter of 2020. In the same period newly originated loans and advances subject to public guarantee schemes increased to €340 billion (from €183 billion in the second quarter). Other loans and advances subject to COVID-19-related forbearance measures (non-expired) remained broadly stable and stood at €50 billion at the end of 2020.

Chart 10

Loans and advances subject to COVID-19-related measures by reference period

(EUR billions)

Source: ECB.

Supervisory banking statistics are calculated by aggregating the data that are reported by banks which report COREP (capital adequacy information) and FINREP (financial information) at the relevant point in time. Consequently, changes in the amounts shown from one quarter to another can be influenced by the following factors: