|

|

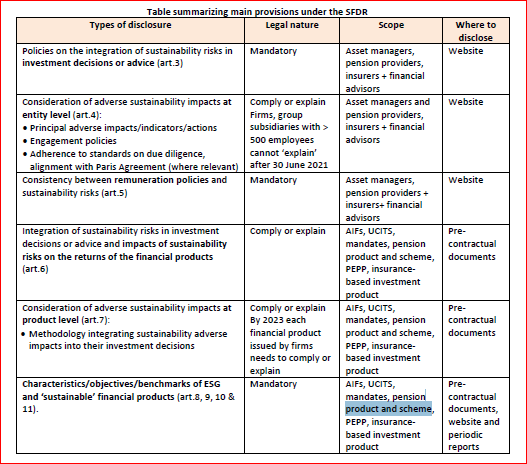

Following the consultation paper of last year (see ICMA AMIC response submitted on 1 September 2020), the European Supervisory Authorities (ESAs) published their final report with recommendations regarding the regulatory technical standards (RTS) for the Sustainable Finance Disclosure Regulation (SFDR).

The ESAs propose to apply the RTS from 1 January 2022, confirming again that the level 1 text will start to apply from 10 March 2021 without the RTS (see ICMA memo summarizing the main provisions of SFDR). A statement by the ESAs is to be issued in the course of February on how to apply the level 1 text from 10 March 2021.

Regarding the RTS, it is now up to the European Commission to decide whether or not to endorse the proposal from the ESAs (decision within 3 months; possibility to deviate from the ESAs’ proposal; and possible 4 weeks consultation prior the EC adoption).