Where do Northern Ireland’s imports come from? Is Northern Irish trade skewed towards ‘checks intensive’ products? What is the current trend in Northern Ireland’s imports?

Tensions over the Northern Ireland Protocol (NIP) have intensified as the UK Government (henceforth HMG) announced plans

to introduce legislation that would enable it to disapply parts of the

Protocol. The UK has often demanded the re-negotiation of the NIP due

to its economic costs, and a too strict application by the EU. Recently,

Assembly elections in Northern Ireland escalated the urgency of

resolving the issue, as the Democratic Unionist Party (DUP) is currently

refusing, as part of its protest against the NIP, to participate in the power-sharing executive.

Given the foregoing, we have examined trade data to shed light on three key issues:

- Where do Northern Ireland’s imports come from?

- Is Northern Irish trade skewed towards ‘checks intensive’ products?

- What is the current trend in Northern Ireland’s imports?

We conclude that with 60% of Northern Ireland’s (NI) imports coming

from Great Britain (GB), the importance of East-West trade is

undisputable. The barriers created by the NIP that affect trade from GB

into NI were always bound to result in shipping delays and higher costs

to trade. In this context, the increase in NI imports from the Republic

of Ireland (RoI) in 2021 could suggest that some firms in NI have

started to find alternative suppliers. However, whether the NIP creates

‘serious economic difficulties’ that are ‘likely to persist’, or a

‘diversion of trade’ (the grounds to invoke Art. 16 of the NIP) is yet

to be determined.

The policy context

To avoid a border on the island of Ireland whilst at the same time

protecting the integrity of the EU Single Market, the NIP placed a

custom and regulatory border between NI and GB. Products moving from GB

to NI must be shown to comply with EU standards which, especially in the

agri-food sector, implies a list of documentary, identity, and physical

checks. These new procedures have resulted

in increased paperwork for firms, likely higher costs to move products

into NI (due to agents’ and hauliers’ fees, and increased staff time),

and longer shipping times.

In response, HMG has recently proposed legislation that would allow

the unilateral suspension of parts of the NIP, to eliminate all checks

for goods shipped from GB intended for exclusive sale within NI and

allow producers of such goods to adhere to UK standards only. Checks on

goods destined for the RoI would be retained, with the identification

of such products the responsibility of traders operating under a

‘trusted trader scheme’. In addition, the UK wants to allow NI

businesses to choose between UK or EU standards, regain the power to

apply UK VAT rates in NI, and reduce the role of the European Court of

Justice in overseeing the NIP. In sum, the UK believes that a

light-touch approach to the border issue is enough to protect the EU

Single Market.

The EU’s response will most likely depend on the extent to which the

UK deviates from the current arrangements (i.e., if some checks are to

be maintained), and the modalities in which the suspension of the NIP

will occur (i.e., either through the legal framework provided by Art. 16

of the NIP or by internal law acts that bypass the obligations in the

NIP). We refrain from analysing the legality of the actions currently

considered by HMG and the possible responses of the EU. Instead, we

examine trade patterns to help situate the dispute over the NIP into an

economic context.

Where do Northern Ireland’s imports come from?

The NIP only affects trade flowing from GB to NI, as in the opposite direction HMG has promised the absence of barriers to GB for NI exporters.[1] Hence, we will focus our analysis on NI goods imports.

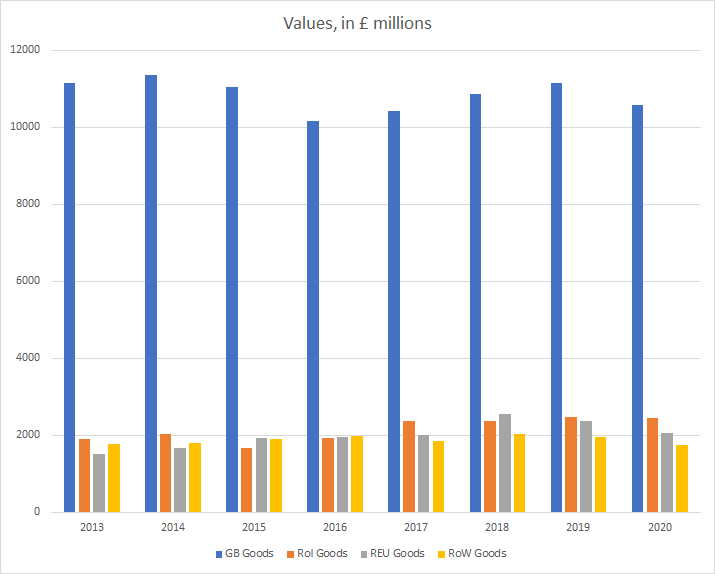

In Figure 1, we use Broad Economy Sales and Exports Statistics

(BESES) data available up to 2020 to depict NI imports from GB, the RoI,

the Rest of the EU (REU), and the Rest of the World (RoW), both in

values and as shares of the total. GB is by far the NI’s largest goods

supplier, with over 60% of NI’s imports sourced from the rest of the UK.

This is salient if compared to the RoI (10-15%), and denotes the

predominance of the East-West trade direction over the North-South one.

However, GB’s share in NI imports has contracted compared to the

pre-2016 referendum years, while that of the RoI and the REU has

correspondingly increased. Overall, the relevance of NI inward trade

from GB helps to understand why HMG is resolved to make trade between

the two regions as frictionless as possible.

FIGURE 1: NI EXTERNAL PURCHASES BY ORIGINS

UK Trade Policy Observatory

© UK Trade Policy Observatory

Key

Hover over the blue highlighted

text to view the acronym meaning

Hover

over these icons for more information

Comments:

No Comments for this Article